Much of the focus of recent antitrust scrutiny has been on companies, with very little attention paid to the motivations of the individual managers setting the anticompetitive strategies of their enterprises. Understanding the concrete personal incentives of the billionaire blockholders entrenched at the helm of most of America’s incumbent corporations is critical to devising effective competition, corporate governance, and tax policy fixes to tackle harmful market concentration at the root.

Meta. Amazon. Apple. Google. Growing antitrust scrutiny—among the antitrust enforcement agencies, the media, and the broader public—has centered on specific businesses engaged in unfair competition or monopolistic practices, such as Amazon preferencing vendors on its online market that pay for its ancillary services like the company’s web services. Yet, the motivations of the corporate managers and CEOs devising those anticompetitive strategies are often treated as irrelevant to antitrust monitoring and enforcement, at best left as a vulnerability for the firms’ boards to consider.

That is a mistake. To understand the underlying motivations of firm managers who pursue monopolistic practices—and the lasting ways to correct them—we must look at their underlying incentive structures.

Let’s start with some stylized facts about the ownership structure of big business today. Seven out of ten of the world’s largest corporations have a billionaire CEO or a billionaire as their principal shareholder, according to recent research by Oxfam International. In the United States, many of the wealthiest Americans either are (or were) simultaneously the founders, CEOs, and chairs of the board of directors of corporate giants, such as with Meta, Berkshire Hathaway, and Nvidia. Not only do these figures control the boards and serve as chief executive, many are also their companies’ largest shareholders, otherwise known as “blockholders.” My colleague Emily DiVito and I recently found that, on average, over one-third of the outstanding shares of the public firms controlled by the top 50 U.S. billionaires are owned by those same billionaires—providing them immense leverage over corporate decisions. Larry Ellison—chair of the Oracle board—alone owns 42% of the company’s stock, and Dan Gilbert owns 70% of Rocket Companies. Many of these owner-managers also hold special voting rights that allow them to veto initiatives by other shareholders.

In the business world, corporate ownership equates to corporate control, as the most shares equates to the most voting rights. So, growing concentration of power at the very apex of the largest businesses allots the individuals who enjoy it extraordinary decision-making authority. Today’s “Great Reconcentration” of stock ownership is eerily similar to the end of the 19th century, when corporate America was largely owned and controlled by a handful of corporations, in turn owned and controlled by a “blockholder oligarchy” of figures who held the simultaneous positions of CEO, board chair, and largest shareholder. As illustrated most recently with Elon Musk’s control over Tesla, the basic system of checks and balances that once may have existed between shareholders and managers collapses once one individual or family simultaneously manages, controls the board of, and owns the largest share blocks in a particular company. This allows these owner-manager-board chairs to almost unilaterally decide the direction of their company, especially on strategic matters such as mergers and acquisitions.

Indeed, we see a remarkable pattern across these billionaire-controlled corporations. Company after company exhibits business models centered on expanding market power and increasingly capturing key economic chokepoints. Using Morningstar’s Moat Index, which measures how impregnable a company is to competition, we found that 27 of the 28 billionaire-owned companies with available data possess an economic moat, meaning that financial analysts see them as able to net excess profits (or rents) well into the future by holding off competition. Sixty-four percent of those 28 firms enjoy a wide economic moat, and so, according to analysts, are likely to produce rents for the next 20 years.

The implicit (and sometimes very explicit) assumption amongst financial analysts is that those firms that can capture rents over time have higher intrinsic value, and thus deserve higher stock prices. As Warren Buffet famously said, “the most important thing [to stock-picking is] trying to find a business with a wide and long-lasting moat around it.”

Connecting the dots here, these anticompetitive moats provide a fundamental source of wealth appreciation for their billionaire blockholder owners/managers. These individuals have both the built-in personal incentives and the personal power over their firms to make their companies as anticompetitive, and thus as profitable, as possible. We found that over 75% of the wealth of the top-50 American billionaires is sunk into the equity shares of the companies over which they have—or had—significant power. These individuals have both a clear financial interest and the leverage needed to boost their companies’ equity prices by reducing competition.

Take Mark Zuckerberg’s Meta Platforms. Zuckerberg—CEO, board chair, and by far the largest shareholder in Meta with special voting rights—holds 96% of his wealth in his company’s stock. It should be unsurprising then that Zuckerberg personally oversaw the company’s legally questionable killer acquisition strategy, in which a firm acquires another company to quash future competition. He argued in one internal email that “it is better to buy than compete.” His wealth at the core depends on the enduring market power of Meta—most recently in the race over control of artificial intelligence.

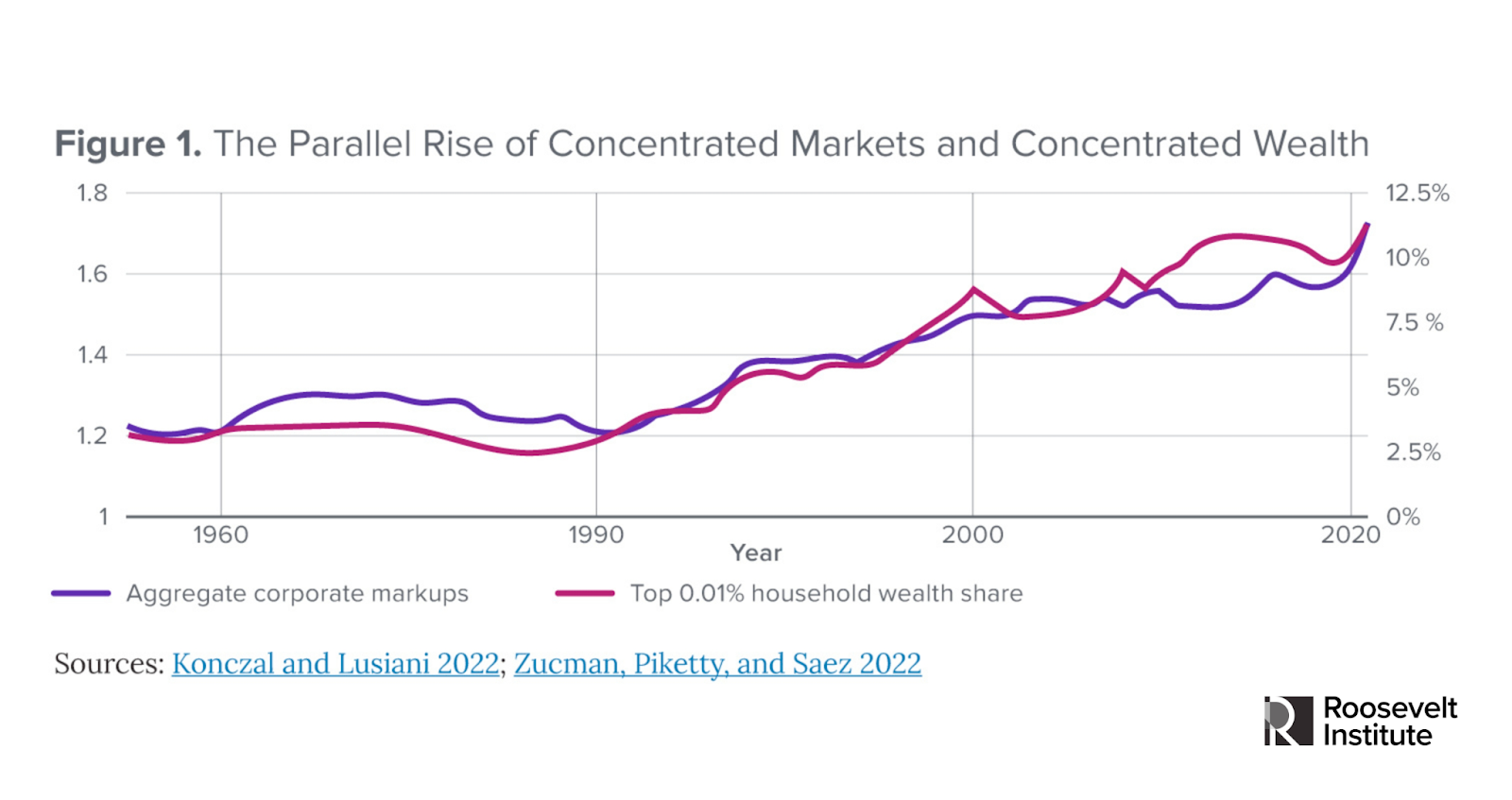

Unlike an earlier era when stock ownership was more diffuse, the “Great Reconcentration” of stock ownership amongst America’s billionaire class makes it more likely that corporate decisions are made in pursuit of the personal interests of those holding those concentrated shares. Zooming out, we see a remarkable parallel rise of market concentration and wealth concentration across the U.S. economy over the past 50 years—suggesting a clear relationship between excessive wealth concentration and excessive market power.

Let me be frank. The financial interests of the billionaire blockholders controlling much of corporate America today are fundamentally misaligned with the interests of a healthy, competitive economy. Smart competition policy and robust antitrust enforcement is helping to help prevent the worst monopolistic practices. But we must also look to corporate governance and tax reforms to tackle market concentration at the root.

Corporate governance reforms need to restore balance within corporations. This would start by disallowing harmful dual-class structures that strip away voting rights from the majority of shareholders and separating conflicting board chair and CEO roles. Unlike billionaire blockholders, most shareholders don’t own three-quarters of their assets in one company. Their diversified portfolios have more to gain from a competitive playing field than markets cornered by a few firms. Mandating worker representation on boards would also help deconcentrate decision-making and broaden the influence of a constituency that sees beyond the next earnings cycle. To align business decision-makers with measures that benefit the economy as a whole, meanwhile, we should redefine corporate purpose and board responsibilities beyond simple shareholder returns and toward the public interest. And to do that effectively, we’ll need to move toward federalizing the corporate charter for the largest corporations to avoid the race to the bottom in corporate law.

As we approach the sunsetting of much of the Tax Cuts and Jobs Act, tax policy also jumps out as a third critical tool. Recent improvements to the tax code in the Inflation Reduction Act, in particular the corporate alternative minimum tax, more robust IRS funding, and the stock buyback excise tax can help level the playing field between large and smaller firms. New bipartisan legislation to end the tax-free treatment for large acquisitive corporate reorganizations would reduce the capital gains tax breaks owners receive by landing merger deals. A billionaire income tax—especially if implemented alongside a global minimum wealth tax on billionaires—could reduce the financial incentives billionaire blockholders receive from monopoly-fueled share appreciation. Returning to a graduated corporate income tax—with a much higher rate on supernormal profits than normal profits—could also help tilt the tax playing field against rent-seeking, high-profit companies relative to their rivals, improve the competitive environment, and reduce the returns to excess profits driven by monopolistic practices by the incumbent companies they control.

In the end, the parallel rise in corporate, wealth, market and stock ownership concentration is not a coincidence but a predictable result of the way laws have been written and our policies conceptualized. Understanding the concrete personal incentives of the billionaire blockholders entrenched at the helm of most of America’s incumbent corporations is critical to devising effective competition, corporate governance, and tax policy fixes to tackle harmful market concentration at the root.

Disclosure: The author works for the Roosevelt Institute, which receives funding from organizations like the Ford Foundation, William and Flora Hewlett Foundation, Omidyar Network, and Open Society Foundations. Read more about our disclosure policy here.

Articles represent the opinions of their writers, not necessarily those of the University of Chicago, the Booth School of Business, or its faculty.