Advertisement

Advertisement

Fed Ramps Up Hawkish Talk; Tech Sells Off, Dip-buyers Return

By:

In what seemed like a dress rehearsal for a more sustained taper tantrum, US markets sold off last week when Fed minutes released from December’s FOMC meeting suggested that the central bank was considering hiking interest rates sooner, and more aggressively, than expected.

Normally FOMC meeting minutes are somewhat of a non-event as the major insights tend to be communicated during the post-meeting press conference. However, this year we’ve had at least two occasions when the release of the minutes has spooked markets into a risk-off mood.

Yields up, stocks down

A combination of soft PMI data, down to 58.7 in December from 61.1 in November, along with a contraction in JOLTS job openings, caused US markets to sell off on Tuesday, January 4. This set the stage for a more pronounced rout on Wednesday when the minutes were released.

The bond market sold off, which had the effect of spooking tech stocks, particularly as 10-year yields rose to 1.764% for the first time since March of last year. Crypto also took a significant hit; the broad market was down by around 6% on the day as investors with paper profits from 2021 begin to weigh how slowing growth and a more hawkish Fed are likely to dampen the enthusiasm for risk assets.

The S&P 500 was down over 1.8% on the day. The Nasdaq 100 fell by around 2.7%, and the Russell 2000 dropped by more than 3.3%.

Sector rotation?

A great deal has been made recently about the fact that the percentage of Nasdaq 100 stocks that are down by 50% or more from their 52-week highs is almost at record highs. We haven’t seen a situation when so many of the index’s stocks are down despite it trading close to highs since the dot-com bubble of 2000.

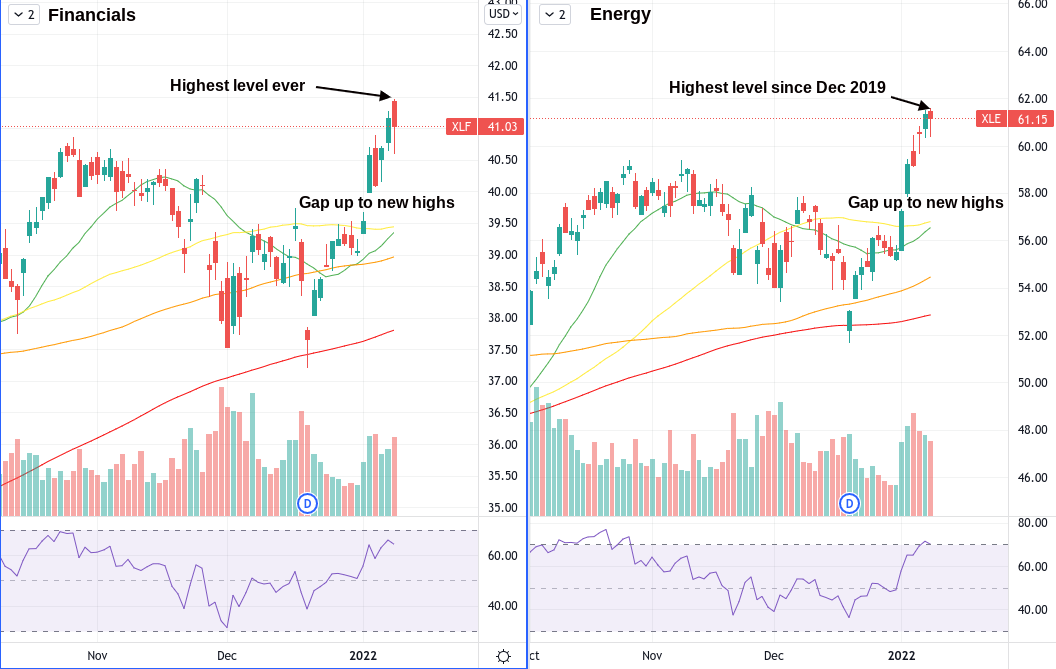

The best performing sectors in the first week of January, following the selloff, were Financials and Energy, up 7% and 4% on the week, respectively. This has caused many to speculate about a broader sector rotation. Whether this proves to be the case or not, you can see the market’s concerns present in this mini rotation. Financials are set to perform well in an environment of rising rates. Also, with inflation concerns still front and centre, and the worst of the winter still not over with, energy seems like a smart bet for many investors.

Tech did not actually lead the selloff. Home construction was the worst-performing US sector last week, down 7.8%. Tech was down 3.8% and real estate down 3.3% on the week.

Dip buyers return on Monday

Monday, January 10, saw a substantial gap down across all major US markets on opening. Dip buyers returned en masse to prevent the Nasdaq 100 from enduring a fifth consecutive session of losses. The rally was larger than any such rebound since the depths of the coronavirus crash back in March of 2020. The move would see the Nasdaq 100 alone trading incrementally higher at Monday’s close than it did on Friday’s.

What the minutes said and why it’s a big deal

The offending comments from these particular Fed minutes went as follows:

“…it may become warranted to increase the federal funds rate sooner or at a faster pace than participants had earlier anticipated. Some participants also noted that it could be appropriate to begin to reduce the size of the Federal Reserve’s balance sheet relatively soon after beginning to raise the federal funds rate.”

Why was this such a big deal? Because up until now all the talk has been around tapering existing asset purchases and getting to a point where the Federal Reserve can begin to start raising interest rates. These minutes go further than the taper that’s currently underway, or the raising of rates at a faster pace (which the Fed has previously signalled).

December’s minutes suggest that the Federal Reserve is considering putting an end to quantitative easing and replacing it with quantitative tightening (active reduction of the balance sheet). When QE (which is by definition accommodative) goes away, financial conditions necessarily tighten and it’s the prospect of this tightening that financial markets are reacting to.

But it’s more than just that. The famous taper tantrum of 2018 took place as the Federal Reserve was reducing the balance sheet (quantitative tightening) at the same time as raising interest rates. Back then, Powell managed to get the Fed funds rate up to 2.5% before a 20% drawdown in US equity markets caused him to pivot. It’s this combination of balance sheet reduction and interest rate hikes that markets are reacting to.

Data to look out for this week

Wednesday’s upcoming CPI reading should hopefully provide more clarity where inflation is concerned. Also, be sure to keep an eye on the EIA’s crude oil inventory report on the same day, and US initial jobless claims on Thursday.

Final thoughts

The question is how much tightening can equity markets tolerate and where will inflation be once this level is reached? Remember, stocks can rise with a tightening Fed as long as growth levels are maintained. Company earnings will be a key factor to watch this week, as any sharp revisions in growth expectations will get investors’ attention and could result in a further slide for stocks.

Tech, energy and financials stocks, indices such as Nasdaq100 and S&P500, as well as other instruments in forex, commodities and other asset classes are all available to trade with HYCM.

by Giles Coghlan, Chief Currency Analyst, HYCM

About: HYCM is the global brand name of Henyep Capital Markets (UK) Limited, HYCM (Europe) Ltd, Henyep Capital Markets (DIFC) Ltd and HYCM Limited, all individual entities under Henyep Capital Markets Group, a global corporation founded in 1977, operating in Asia, Europe, and the Middle East.

High Risk Investment Warning: Contracts for Difference (‘CFDs’) are complex financial products that are traded on margin. Trading CFDs carries a high degree of risk. It is possible to lose all your capital. These products may not be suitable for everyone and you should ensure that you understand the risks involved. Seek independent expert advice if necessary and speculate only with funds that you can afford to lose. Please think carefully whether such trading suits you, taking into consideration all the relevant circumstances as well as your personal resources. We do not recommend clients posting their entire account balance to meet margin requirements. Clients can minimise their level of exposure by requesting a change in leverage limit. For more information please refer to HYCM’s Risk Disclosure.

About the Author

Giles Coghlancontributor

Giles Coghlan is a Chief Currency Analyst and has been consulting for HYCM Group since April 2018. Giles plays a key role by internationally representing the Group and providing his expertise to HYCM’s investors.

Did you find this article useful?

Latest news and analysis

Advertisement